Mortgage Rates Will Move. Serious Buyers Prepare Anyway.

Mortgage rates have been anything but steady lately, and that kind of movement can make planning feel more difficult for buyers trying to make a smart decision.

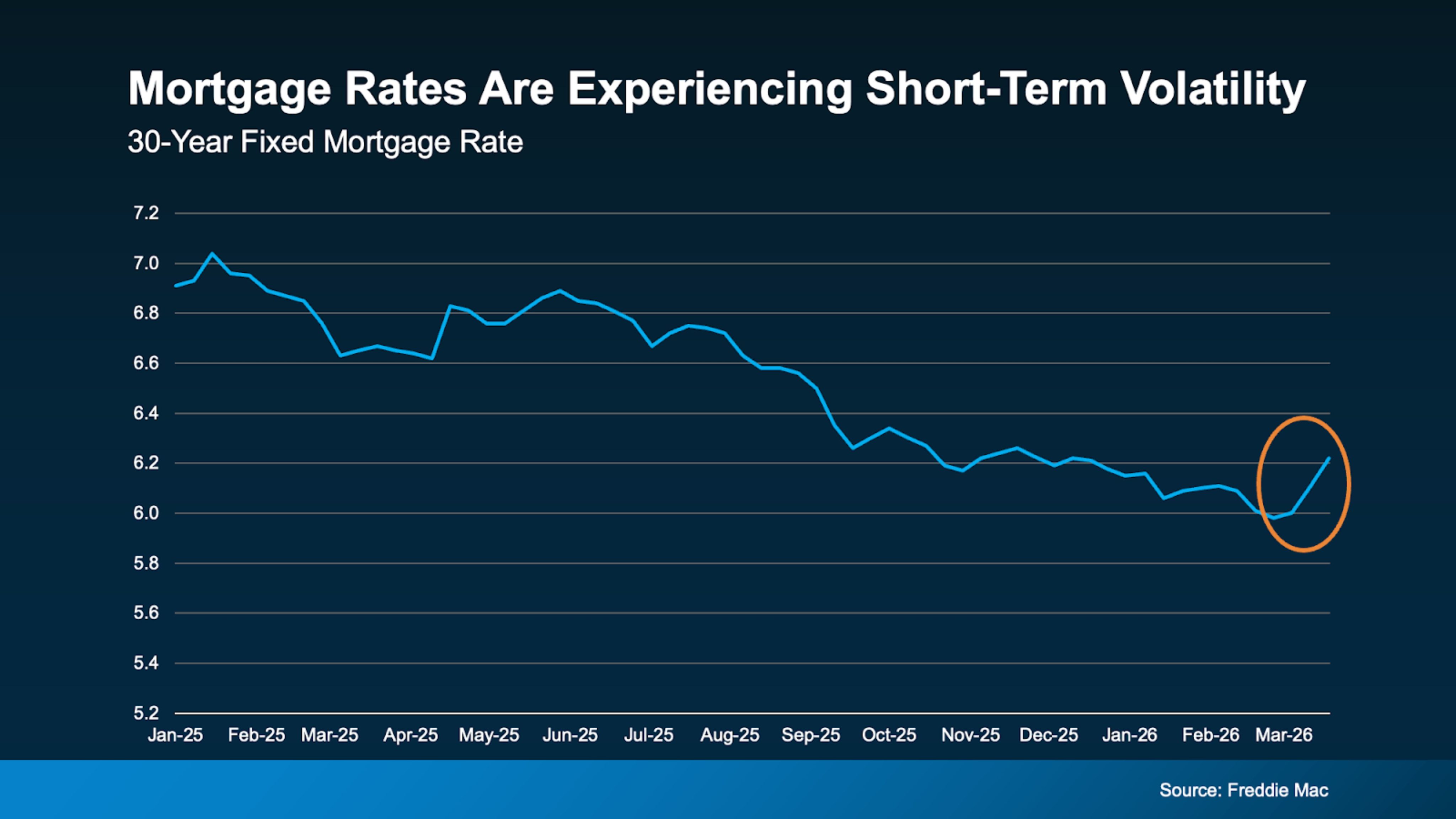

When rates shift, it is easy to get distracted by the headlines and assume the right move is to wait until things settle down. But the truth is, short-term movement in mortgage rates is not unusual. It is part of how the market works.

Mortgage rates do not move in a straight line. They rise, dip, and adjust in response to broader economic conditions, and that kind of short-term movement is normal.

Even in recent months, rates have shifted up at times before moving back down again. That is why buyers should avoid reacting to every change and stay focused on long-term readiness instead.

Periods of economic uncertainty and major global events can add even more volatility, which is one reason trying to time the market rarely works. What matters more is being prepared to act when the right opportunity appears.

If you want, I can make it even shorter so it fits more cleanly under the chart.

Strengthen Your Financial Position

Your financial profile plays a larger role than most buyers realize. It is not just about getting approved. It is about how favorable your terms can be once you are.

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions. Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That means even small improvements can create real advantages. A stronger credit score, a healthier debt-to-income ratio, and more financial stability all work in your favor when lenders evaluate your application.

This is where preparation becomes practical. Understanding where you stand today gives you a clearer path to improving your position before you need it.

Choose the Right Loan Approach

Not all home loans are structured the same way, and the one you choose can have a meaningful impact on your rate, your monthly payment, and your overall flexibility.

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

This is why loan strategy matters. The goal is not just to secure financing. It is to choose a loan structure that aligns with your budget, timeline, and long-term plans.

The right lender can walk you through your options and help you understand what makes the most sense for your situation, not just what gets you through the door.

Look Beyond the Interest Rate

Mortgage rates tend to get the most attention, but they are only one part of the bigger picture.

“The length of your loan matters too. Most lenders typically offer 15, 20, or 30-year loans. When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

A lower rate may sound appealing at first, but what matters more is how the full loan structure fits into your life. Monthly affordability, total interest paid over time, and long-term flexibility all deserve equal attention.

Buyers who focus only on the rate often miss what matters most. Buyers who understand the full cost of the loan are in a stronger position to make a smart, confident decision.

Preparation Creates Leverage

Too many buyers stay on the sidelines waiting for rates to drop before they begin the process. But hesitation is not always a winning strategy.

By the time rates improve, the market may look different. Competition can increase. Inventory can tighten. Pricing can shift. And suddenly the advantage buyers were waiting for gets offset somewhere else.

The stronger approach is to prepare before the perfect moment ever shows up.

That means knowing your numbers, understanding your options, improving what you can improve, and putting yourself in a position to act with confidence when the right home becomes available.

The buyers who move well in this market are not the ones who predict every rate shift correctly. They are the ones who are ready when opportunity appears.

BOTTOM LINE

Mortgage rates may continue to fluctuate, and Freddie Mac’s latest survey showed the average 30-year fixed rate rose to 6.38% on March 26, 2026, up from 6.22% the week before. That kind of movement reinforces the central reality buyers are facing right now: volatility is part of the market, and waiting for perfect certainty is rarely the winning strategy.

What matters more is preparation. Buyers who understand their financing, strengthen their position early, and move with a clear plan are better equipped to respond when the right opportunity appears. In a market shaped by shifting affordability and changing conditions, strategy creates confidence.

Across North County San Diego, that kind of guidance matters. Shafran Realty Group serves buyers and sellers throughout Carlsbad, Encinitas, Oceanside, Vista, San Marcos, and surrounding communities, with Alan Shafran positioned by his brokerage as a Carlsbad expert and recognized by The Wall Street Journal as one of the Top 100 Realtors Nationwide and the #1 Realtor in San Diego County.

If you are thinking about making a move, the right response to rate volatility is not guesswork. It is a smarter plan, grounded in preparation, local insight, and the confidence to act when the timing is right for you. Connect with Shafran Realty Group for guidance built for the North County San Diego market today.

Check out this article next

What To Do When Your Home Isn’t Getting Offers. Read This.

When homes are not receiving offers, the issue is often not demand but how the property is positioned in today’s market. With buyers becoming more…

Read Article